Synopsis: India GCCs are not limited to just big companies anymore, small and medium-sized enterprises are also rapidly moving towards getting their GCCs set up. By 2030, the mid-segment will set up more than 900 GCCs. This article gives a comprehensive analysis of the Mid-segments.

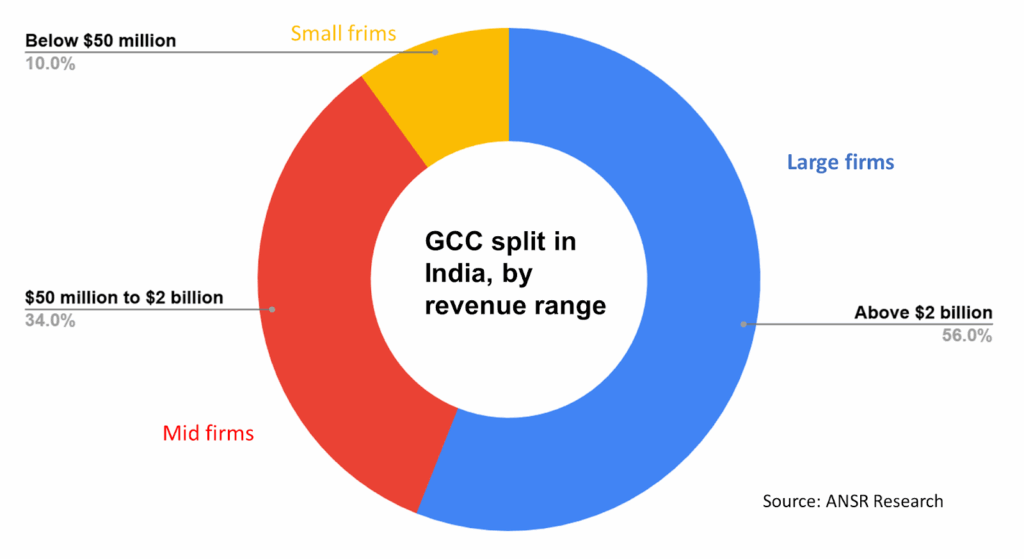

As per the ANSR Research report, India has 610 mid-segment Global Capability Centres(GCCs). North America contributes the largest share with 448 GCCs, followed by Europe with 114, Asia Pacific with 20, and the rest of the world with 5. These centres together account for a whopping $14.23 billion annual revenue and hire almost 462,000 employees.

Mid-segment firms represent approximately one-third of India’s GCC ecosystem, and they have increased from 492 in 2020 to more than 610 now. Such consistent growth is indicative of their increasing significance in the digital and operational domains of India. In the future, it is foretold that more than 950 mid-segment GCCs will be located in India by 2030.

Major mid-segment GCC cities in India

Bengaluru is always shining for attracting GCC to India, with 205 out of the total 610 new ventures and having a talent pool of 166,000 professionals. This figure is equivalent to 34% of all the GCCs of the emerging enterprises that have been studied, which is a huge concentration that indicates the city’s steepness, density of the ecosystem, and the fact that the talent density is still an irreplaceable advantage of the city.

Hyderabad, which at present has less of the emerging segment in the number of companies, is nevertheless the fastest of all the metros in terms of new GCC investments as well as the closest to Bengaluru in terms of new traction. The city has today become a leader in new GCC establishment rates due to the combination of aggressive government incentives, state-of-the-art infrastructure in HITEC City and the Financial District, and a specialized talent pool that is rooted in pharmaceuticals and cloud platforms.

Another 44 emerging enterprise GCCs with roughly 47,000 workers are shared among Delhi-NCR, Pune, Mumbai, and Chennai. Each of these cities has its own specializations. Mumbai retains its position as the BFSI center, Chennai has the edge in enterprise SaaS operations, and Pune is becoming a mixed-breed innovation hub.

The Emergence of Tier-2 Cities

The biggest geographic headline is the emergence of India’s tier-2 cities that are just beginning to open up, as they account for a combined 14% of all emerging enterprise GCCs. Cities like Ahmedabad, Coimbatore, Kochi, Trivandrum, Vizag, Jaipur, and Indore are transforming very fast from being just regional outposts to being capable of providing strategic support.

- Cost Efficiency: Tier-2 cities boast a total cost of operations that is lower by 10-35% in comparison with tier-1 metros, the major factors being cheap commercial real estate, reasonable wage expectations, and less infrastructure expenses, respectively.

- Hiring Momentum: There is an increasing trend in job advertisements in the Tier 2 GCC hubs, which is evidenced by a 21% increase in job postings compared to the previous year, while in metropolitan areas, the growth was only 11%.

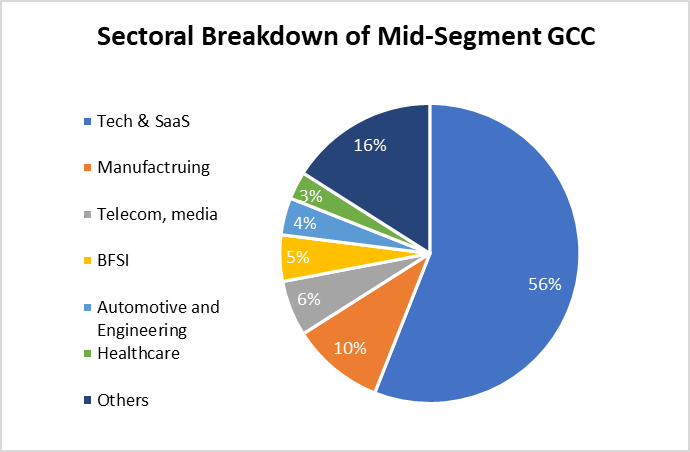

Sectoral Breakdown

Technology & Software/SaaS

GCCs opening up in India for product engineering, AI/ML, and platform innovation are led by Nasuni, New Relic, and Planview. These centers are conducting digital transformation at a global level through IP generation and fast product development, making the world their absolute biggest hub for these activities.

Manufacturing & Industrial

Maxcess, Husco, Stahl, and Lutron design their GCCs for engineering, supply chain, and digital manufacturing. By applying Indian technical talent, they create and lead the 4.0 transformation in the global market.

Telecom, Media & Entertainment

GCCs set up by Traveloka and Bernhard Schulte Shipmanagement are utilized in the areas of platform development, customer service, and content technology. The companies benefit from the centers’ support in the areas of digital service scalability and global media-tech competence.

BFSI

SmithHoward, D360, Brit, Onity, and Saxo Bank hire skilled employees for their GCCs, focusing on fintech innovation, risk analytics, and digital banking solutions. These areas include regulatory technology, alternative investments, and the development of decision systems that operate in real-time.

Also read: Why India Is the Top GCC Hub for Emerging Enterprises in 2026

Automotive & Engineering

The companies ETAS, Normet, and Hoerbiger focused on automotive software, engineering simulation, and connected vehicle platforms. Their global centers are mostly concerned with the invention of embedded systems and the development of electric vehicle (EV) technologies.

Healthcare & Lifesciences

The companies RxBenefits, Nextgen, ModMed, and ClinChoice are amongst those who are establishing global development centers(GCCs) for revenue cycle management, health tech platforms, and clinical research. They are mainly concentrating on the areas of AI-driven drug development and telemedicine infrastructure.

Others

Retail/CPG like Mercar, Groupon, Logistics (RLogix), and Semiconductors are utilizing GCCs for e-commerce platforms, supply chain AI, and chip design. These various industries take advantage of specialized domain expertise at optimized costs.

Conclusion

Mid-segment GCCs are the next big thing in India’s GCC market and are expected to grow to 950 centers with a workforce of 700,000 professionals by the year 2030. The whole trend is from Bengaluru’s superiority to the quick rise of tier 2 cities, where the mid-market angels are the ones to push the AI transformation and the creation of value, which is not only through cost arbitrage.

Written by Yatheendra N