Synopsis: A dramatic shift is underway in India’s real estate market, with the retail sector expected to capture 30% of the market by 2030. This article explains the top emerging retail real estate segments, the fastest-growing cities, and the key reasons driving this growth.

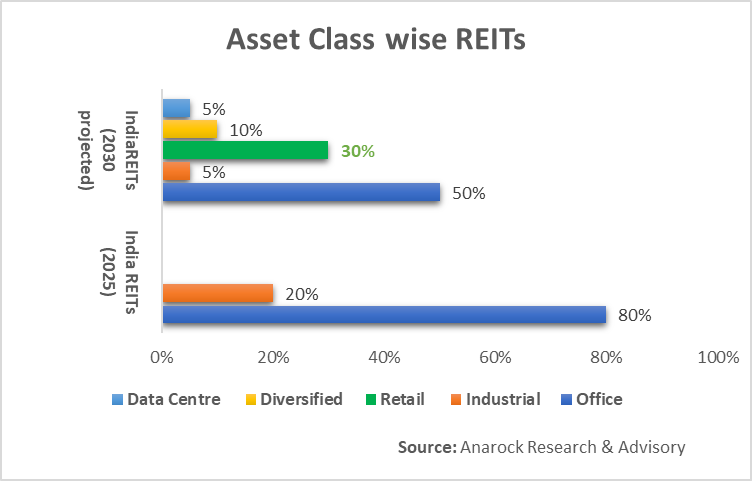

The Indian retail real estate sector is undergoing a structural change, moving from a fragmented market to a highly organised, institutional asset class. As you correctly identified from the data, the sector is projected to see a massive growth, expected to capture 30-40% share of India’s total REITs market by 2030. According to the JLL reports, between 2025 and 2030, India’s retail sector is poised to witness its largest ever infusion of mall supply, with approximately 60.9 million square feet of new retail space entering the market. This is not incremental growth, it’s a structural reimaging of urban retail landscapes across the country.

The Scale of Transformation

In the past four years, 60 international brands have entered India, with new entrants nearly doubled from 14 in 2023 to 27 in 2024. Developers have noticed this trend and are augmenting the supply of REIT able mall spaces steadily. Over 16.6 million square feet of Grade A mall space is expected across the top seven cities by the end of 2026 alone, with Hyderabad and Delhi-NCR accounting for nearly 65% of this retail expansion.

This surge is being led by listed real estate developers Nexus Malls (backed by Blackstone). Phoenix, DLF, Prestige Estates, and Lakeshore Realty which collectively control over 58 operational malls spanning 34 million square feet and have more than 45 new malls in their development pipeline. Currently, only one listed retail REIT exists Nexus Select Trust, backed by Blackstone—but Anarock Research forecasts that 2-3 new retail REITs will launch within the next three to five years as developers consolidate quality portfolios for listings. This will position retail REITs to eventually command ₹60,000-₹80,000 crore of value by 2030.

Fastest Growing Retail Cities in India

The growth is no longer limited to Delhi, Mumbai, and Bengaluru. A “consumption explosion” in non-metro cities is widening the retail map.

- Hyderabad: Currently the standout performer, it accounts for over 70% of total retail leasing activity. The HITEC City and Kondapur areas are seeing massive retail demand from tech-affluent consumers.

- Delhi-NCR & Mumbai: These cities continue to anchor the market, with Mumbai registering 1.6x year-on-year growth in leasing. They are the launchpads for international brands entering India.

Also read: 5 Fast-Rising Karnataka Cities Beyond Bengaluru That Will Become the Next Big Hotspots by 2032

The Tier-II Story

Indore, Lucknow, Chandigarh, Jaipur, Kochi, Coimbatore, and Bhubaneswar are now welcoming the first-time institutional developers. These cities have the best of everything – the rise in disposable income, improvement in infrastructure and, and most importantly, the craving for branded retail and lifestyle experiences.

Over the next five years, new retail in Tier-II and Tier-III cities together are going to be more than 25 million square feet. The number of branded fashion stores in Indore alone increased by 46% in 2024, whereas the number of Food & Beverages launches in Tier-II cities increased by 25-26%, which is indicative of the consumers wanting more of the high-end items.

The Four Pillars Driving Growth

1. Premiumization and Experience-Led Retail: The “super rich” annual income of ₹1 crore+ population is increasing at the rate of 14 to 18% per year, and the near-affluent households (income of ₹30 lakh+) are growing at 7-11%. The modern malls have now converted into social hubs by majorly 30 to 40% dedicating their space to F&B, entertainment, and lifestyle zones rather than just shopping destinations.

2. International Brand Influx: The global retailers’ entry has been very rapid. Over 60 international brands have come to India in the last four years, with 27 new ones in 2024 alone. From high end brands like Louis Vuitton, Panerai, Eleventy to lifestyle (Lululemon, Bershka, Nespresso), international players are heavily pursuing India’s expanding consumer market. This trend has set off a chain of events leading developers to construct the Grade A properties that are complying with the global operational standards that the REIT investors demand.

3. D2C (Direct-to-Consumer) Brands: One of the unique cases in India is the rise of the digital-first brands that are looking for the best physical locations for their products. D2C brands have already taken up the best locations in malls as a result of their data-driven customer insights, strong funding, and high trading densities which make them a great asset for mall developers. Snitch, Minimalist, and Rebel Foods are just a few of these brands that are leading the way.

4. Organized Retail Penetration: The organized retail in India at present accounts for merely 12% of the retail market, which is $1 trillion, this being significantly lower than the 80% penetration in developed economies. The huge gap between the two is what drives the growth. Over the next ten years, organized retail sales in India are predicted to go up to ₹19,70,870 crore ($230 billion) with a 10% CAGR. As malls are changing from just quantity-driven to quality-focused collection.

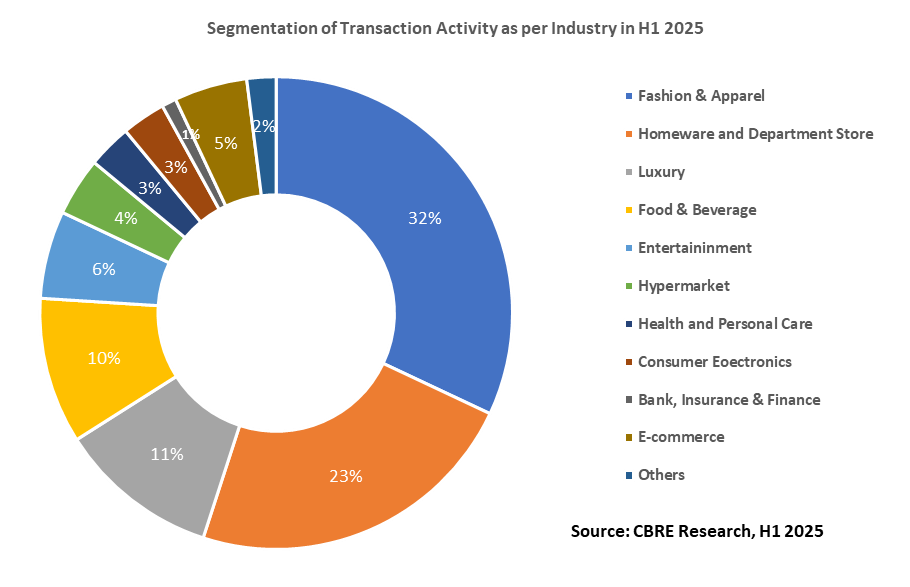

In the first half of 2025, fashion and apparel leasing accounted for 32% of total retail leasing, home and department stores for 23%, and luxury (primarily led by jewelry brands) for 11%.

- Fashion & apparel is gradually falling as online shopping eats into mass-market clothing demand.

- Homeware and department stores take 23%, emerging as big winners as people spend more on homes and lifestyle products.

- Luxury dominates prime high streets, driven mainly by branded jewelry and premium fashion as richer consumers trade up.

- Food & beverage is the fastest‑growing piece, because malls are adding more restaurants and cafes to boost footfall and dwell time.

- The remaining categories entertainment, hypermarkets, health & personal care, electronics, financial services, e‑commerce, and others make up smaller shares but together show how malls are diversifying beyond pure shopping into services and experiences.

Conclusion

By the year 2030, the Indian retail property market would have undergone a complete transformation. It would have shifted from a sector that was not only developer-dominated but also fragmented to a diversified institutional asset class with substantial portfolios controlled by REITs, Grade A malls making up 60% of total inventory, and Tier-II cities being almost on par with metros in the aspect of growth dynamism.

Written by Yatheendra N