Synopsis: Bank fraud cases in India fell sharply by 34% in 2024–25, reflecting a strong monitoring by banks. However, the total amount involved doubled as per RBI reports.

According to the RBI report, the total number of frauds went down. Nevertheless, the money involved in fraud went up. This was mostly because the reexamination and the reporting of 122 fraud cases that amounted to ₹18,336 crore were done afresh after compliance with the Hon’ble Supreme Court’s judgment had been assured.

| Metric | 2023-24 | 2024-25 | Trend | Reason |

| Number of Cases | 36,052 | 23,870 | Decreased | Better real-time detection of digital fraud |

| Amount | ₹16,502 Cr | ₹34,771 Cr | Increased | Includes ₹18,336 Cr from just 122 old cases re-reported due to a Supreme Court order |

In the case of fraud happening, the card/internet frauds accounted for 66.8 percent of the total in terms of the number of cases, during 2024-25. In the case of money, the percentage of fraud related to advances was 33.1 percent.

Private vs Public Banks

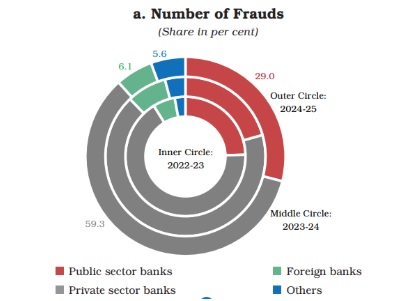

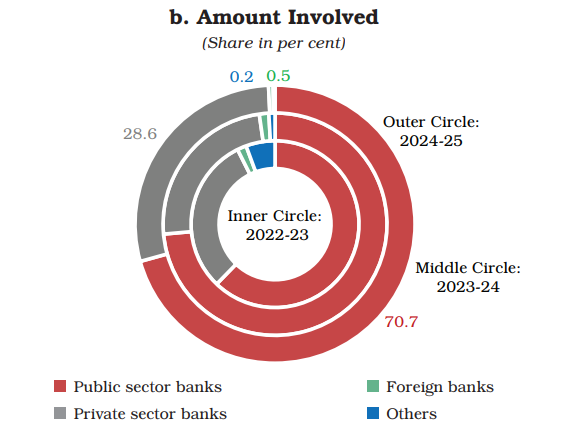

During the 2024-25, fraud in the private sector banks was reported as 59.3 percent of the total, whereas public sector banks were reported as 70.7 percent in the amount involved. Card/internet-related frauds were the largest by number among PVBs, but frauds concerning advances were the largest by value in 2024-25.

On the other hand, public sector banks showed a high rate of advances-related frauds, both in number and amount. There was a decline in the share of card/internet fraud in all the bank categories in 2024-25, both in number and amount.

The share of fraud related to advances, both by number and amount, increased in all bank categories, except for PSBs in terms of amount, which was mainly because a large part of the reclassified frauds was associated with advances.

Also read: Why Global Investors Are Placing $15 Billion Long-Term Bet on India’s Banking Sector

How Modernization is Working

1. The “FREE AI” Framework: In August 2025, the RBI rolled out the Framework for Responsible and Ethical Enablement of AI (FREE AI).

- Impact: The banks are transitioning from “rule-based” detection, like marking transactions over ₹1 lakh, to “behavioral” detection.

- Result: This practice is working especially well against Card/Internet fraud, which constitutes 66.8% of the total fraud cases by volume, but is being caught more quickly, thus preventing large losses.

2. Digital Infrastructure Hardening (.bank.in): To address phishing and spoofing, where scammers set up imitation bank websites, the RBI has proposed the use of exclusive, restricted domains such as .bank.in and .fin.in.

- Why it helps: In contrast to .com or .co.in, these domains are accessible only to recognized financial entities, so it becomes extremely difficult for fraudsters to establish and run believable fake banking sites.

3. Principle-Based Authentication (Effective April 2026): The document observes a transition to an advanced authentication structure. Rather than depending only on SMS OTPs, which can be swapped off through SIM swapping, banks are investing in multi-factor authentication that features “something you are” (biometrics) and “where you are” (geolocation), thus making remote account hijacking considerably tougher.

Conclusion

The drop in the number of frauds in 2024-25 is a “proof of concept” that Digital Payments Intelligence Platform (DPIP) and AI monitoring are effective. The noticeable increase in value is a legacy cleanup, not a new crisis. While the system is more open about past corporate bankruptcies, it is still becoming safer for the typical retail customer.

Written by Yatheendra N