Synopsis: The data centre capacity in India is projected to increase drastically from last year’s figure of 1.4 gigawatts (GW) to 9GW in 2030, thereby consuming about 3% of India’s power consumption in 2030, which is an increase from less than 1% at present. The issue is to provide support for this huge demand in a sustainable manner, and the solution is battery storage along with renewable energy.

As data centres in India continue to expand, their power consumption will rise sharply, creating a greater demand for energy generation. Traditional sources like hydro and thermal power are no longer sufficient to meet this growing need. As a result, renewable energy has become essential, driving increased investment in sectors such as solar and wind power.

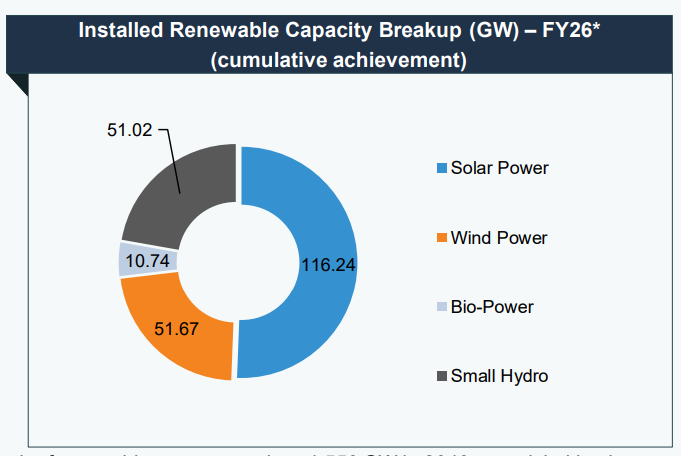

India is planning to reach 500 GW of renewable energy capacity by 2030, with a solar power contribution of 280 GW being the major source. This ambitious target will also open up opportunities for investments amounting to US$221 billion by 2030.

According to the Indian Wind Turbine Manufacturers Association (IWTMA) reports, India’s wind energy sector is progressing considerably towards realizing the ambitious goal of 100 GW of power generation by the year 2030. Presently, the country has a capacity of generating more than 50 GW of installed wind power and a yearly domestic production capacity of over 18 GW for wind turbines and their parts.

Impact of Renewable Energy Investment on Data Centres in India

- Operational Cost Stability: Energy accounts for 30-40% of a data center’s operational expenditure. By shifting to captive renewable energy or long-term Power Purchase Agreements (PPAs), data centers lock in power cost at ₹3-4/ unit, shielding themselves from fluctuations in grid tariffs which can be significantly higher which is ₹7-10/unit).

- Regulatory compliance & ESG Goals: With India’s target of Net Zero by 2070 and the “Green Data Centre” rating systems, operators are forced to prove green sourcing to attract hyperscale clients (Google, Amazon, Microsoft) who have their own stringent 24/7 carbon-free energy goals.

- Infrastructure Reliability: New investments often include hybrid setups combined of Solar, Wind and Battery Storage, which improve uptime reliability compared to pure grid dependence, especially in states with grid volatility.

Also read: Top 10 Major Companies Fueling India’s Rapidly Growing $30 Billion Data Centre Industry

How Data Centers Fulfill their Energy Requirements

Data centers in India currently utilize a mix of four primary mechanisms to fulfill their clean energy needs

| Fulfillment Mechanism | Description |

| Captive Power Plants | Operators build their own solar/wind farms and wheel the power to the data center. |

| Open Access PPAs | Entering long-term(15-25 years) agreements with third party Independent Power Producers (IIPs) to buy green power via the grid. |

| Green Tariffs | Though this is often more costly than the captive routes, the premium paid to the state DISCOMs for sourcing green power directly from the grid is still justified. |

| Renewable Energy Certificates | Acquiring certificates to counterbalance carbon emissions when the sourcing of green power directly is not possible. |

Andhra Pradesh: Data Centre Policy 4.0

By 2030, Andhra Pradesh is the strongest candidate to be the leader in India’s data center growth with the capacity of 6,000 MW and the support of huge investments from Google & Adani.

- 100% Duty Exemptions: The policy grants an impressive 100% exemption for hyperscalers on the electricity duty, transmission charges, and renewable cross-subsidy charges for a span of 15 to 20 years. This means huge direct cost reduction.

- Power Tariff Concession: The policy gives a concession of ₹1 per unit on power tariffs for 15 years, thus cutting down the “burn rate” for power-hungry AI workloads significantly.

- Renewable Energy “Banking”: The policy is in line with the Integrated Clean Energy (ICE) Policy 2024, thus enabling data centers to “bank” the excess renewable energy produced during the day and take it back at night, which is a vital aspect for 24/7 operations.

- Green Hydrogen & Storage: The incentives are associated with the adoption of advanced storage and green hydrogen, thus making AP the prime location for “Green Hydrogen Ready” data centers.

Also read: 7 Leading Investment Firms Betting Big on India’s Growing Data Centre Market

New Investment in Renewable & Clean Energy (2024-25)

| Date | Company | Project Details |

| Oct 2025 | AdaniConneX & Google | $15 Billion Partnership: Announced in Oct 2025 to develop India’s largest AI data center campus in Visakhapatnam, AP. |

| Oct 2025 | Raiden Infotech (Google Backed) | ₹87,520 Crore Investment: Approved by AP State Investment Promotion Board. Includes a massive 1,000 MW capacity in Vizag and Anakapalli. |

| June 2024 | CtrlS Data Centers | GreenVolt1(125 MWp): Commissioned a captive solar farm in Nagpur in mid-2024. It now powers 30% of their Mumbai campus, scaling to 60% by 2025. Part of a plan to build 1 GW of solar capacity. |

| Feb 2024 | Nxtra by Airtel | 140,208 MWh Procurement: Signed new deals to source additional RE via captive plants in Tamil Nadu both Wind and Solar energy and in UP only Solar. |

Conclusion

In Andhra Pradesh, the “Policy 4.0” era (2024–2029) effectively treats data centers as essential power infrastructure. The policy will eliminate transmission and wheeling charges, which usually account for 20-30% of the cost of open-access electricity, thus removing the greatest obstacle to the use of renewable energy.

Written by Yatheendra N