Azad Engineering IPO Review: Companies in the Aerospace and defense industry have been welcomed grandly on the Stock Market with bumper listing gains. Just take the example of MTAR Tech and Paras Defense. Both of them were listed, showering gains of 77% and 180% respectively. In this article on Azad Engineering IPO Review, we shall see about the company, financials, Key Players in the market and much more.

Having said that, we would like to introduce you to yet another opportunity. The Company Azad Engineering is coming up with its IPO issue of Rs. 740 Cr which will open on 20th December 2023. The issue will close on 22nd December and will be listed on the exchange on 28th December 2023.

Azad Engineering IPO Review

About the Company

Azad Engineering is a manufacturer & supplier of key components to Original Equipment Manufacturers in the energy, Aerospace, Defense, and O&G space.

The Company supplies various OEMs across the USA, China, Europe, Japan, and the Middle East. Azad’s Marquee customers are General Electric, Honeywell International, Mitsubishi Heavy Industries, Siemens Energy, Eaton Aerospace, and MAN Energy Solutions SE.

Azad manufactures 3D rotating and stationary Airfoil/blade portions of turbine Engines. These products find application in gas, nuclear, and thermal Turbines. In the Aerospace segment, it manufactures components for Auxiliary Power Units, engines, and hydraulics for commercial and defense aircraft.

The Company has 4 manufacturing facilities in Hyderabad, Telangana of Approximately 20,000 sq meters. Additionally, the Company is adding two more manufacturing facilities with a combined capacity of 1.7 Lakh sq Meters.

As of FY23, Azad Engineering earned 87% of its revenue from the Energy segment, specifically from the Airfoil/blade. Aerospace & defense made up for 8.95% of revenue with Air Generation Systems bringing the last chunk of the revenue. Oil & Gas brought in just 0.02% of revenue in FY23.

About the Industry

The Global Energy Turbine Components Market (which constitutes 72% of the Company’s revenue) was valued at Rs. 28,325 Cr in FY22 and is expected to reach Rs. 28,270 Cr in FY27 The market for nuclear turbines is expected to grow at the rate of 8% CAGR, followed by gas turbines at the rate of 1% until 2027.

Moreover, the Aerospace and defense components market was valued at Rs. 99,000 Cr in FY22 and is expected to reach 1.5 Lakh Cr by FY27, growing at a CAGR of 9%. The overall addressable market for the Company is expected to reach Rs. 1.81 Lakh Cr by 2027.

India has traditionally been a foreign trade deficit nation. The country’s exports have increased at a pace of 9% CAGR in the past 5 years. Engineering products segments have grown at a CAGR of 6.3% from FY18 to FY23.

Iron and Steel account for the largest share or 22% of the total Engineering exports. Industrial Machinery and Aircraft and spacecraft parts account for just 18% and 1% of the Engineering exports respectively, which is the niche market that Azad caters to.

The industry looks optimistic with new developments in India’s foreign trade policy 2023, and a couple of other initiatives by the government such as Make In India, Atmanirbhar Bharat, and Production Linked Incentives (PLI).

Azad Engineering IPO Review – Financials

Azad reported a revenue of Rs. 252 Cr in FY23, which increased by 29.42% from Rs. 194 Cr in FY22. Revenue growth has been really strong growing at 43% CAGR in the past 3 years.

However, Net Profit has failed to replicate its revenue trends. In FY23, the Company reported a Net Profit of just 8.5 Cr, which was a 71% drop from Rs. 29 Cr in FY22. The sudden drop in Net Profits came as a result of an increase in Finance Costs of Rs. 52.3 Cr or 21% of FY23 revenue.

We can estimate that the next year’s finance costs would have reduced significantly, as a result of repayment of debt from the Net Proceeds of the IPO.

The Company’s Cash Flow from Operating Activities (CFO) is Rs. -10.20 Cr as of FY23, due to a steep increase in Trade Receivables and inventory. CFO denotes the profits that are being converted to cash and FY23 figures suggest a pile-up of inventory and money yet to be received from vendors.

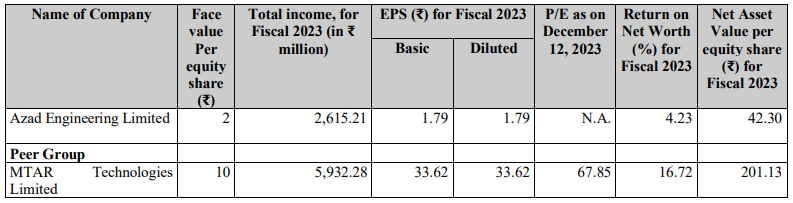

As of FY23, the Company had a return on Equity of 4.23%, with a return on Capital Employed of 12.99% and a debt-to-equity ratio of 1.47x.

Key Players

When we compare Azad against its listed peers, we find that in terms of revenue, Azad is the 2nd smallest on the list just behind Paras Defence. In terms of Earning Per Share Azad is the smallest player among its peers.

If we take the issue’s maximum price and divide it by the Earnings Per Share, we will reach an exorbitant valuation of 292.73x Price-to-earnings. This makes Azad the most overvalued stock.

Nevertheless, the PE valuations are set to come down as the Company’s Finance costs decrease as a result of the prepayment of borrowings.

Strengths of the Company

- The Company operates in a highly engineered market where some of the products offered by the Company come with a Zero Defect Policy. This makes the Company’s expertise in manufacturing products highly critical.

- As per Azad’s RHP, the Company’s client acquisition is done in 4 Phases which can take up to 30 – 48 months. This lengthy acquisition period increases any competitor’s barriers to entry.

- The Company is undergoing a massive capacity expansion fuelled by internal accruals (Retained Earnings). This shows signs of strong demand that the Company might want to cater to.

- The Company has long-standing relationships (Over 10 years) with some of the most notable global OEMs such as General Electric and Mitsubishi Heavy Industries.

Weaknesses of the Company

- The Company earned 65% of its FY23 revenue from its Top 10 customers, of which 33% came from its biggest spender. This kind of revenue stream gives rise to concentration risk.

- Azad imports ~50% of its entire raw materials. Its Top 3 suppliers cost 50% of revenue and its No. 1 supplier costs 25% of revenue. Any fluctuation in foreign currency can significantly impact earnings

- The Company heavily relies on exports, which made up 80% of revenue in FY23 and 90% in H1FY24. The Company relies heavily on Japan & USA, which bring 35.47% and 23.01% of revenue respectively.

- In FY23, the Company’s Net CFO slipped into the negative due to a rise in Inventory & Trade Receivables. These give rise to liquidity risks in the Company.

Azad Engineering IPO Review – GMP

The shares of Azad Engineering Ltd traded at an 83.97% premium in the grey market on December 18th, 2023. The shares in Grey Market traded at Rs 964. This gives it a premium of Rs 440 per share over the cap price of Rs 524.

Key IPO Information

| Particulars | Details |

|---|---|

| IPO Size | Rs. 740 Cr |

| Fresh Issue | Rs. 240 Cr |

| Offer for Sale (OFS) | Rs. 500 Cr |

| Opening date | 20 December 2023 |

| Closing date | 22 December 2023 |

| Face Value | Rs. 2 |

| Price Band | Rs. 499 - 524 |

| Lot Size | 28 Shares |

| Minimum Lot Size | 1 Lot (28 Shares) |

| Maximum Lot Size | 13 Lots (364 Shares) |

| Min. Investment | Rs. 14,672 |

| Listing Date | 28 December 2023 |

Promoters: Rakesh Chopdar

Book Running Lead Manager: Axis Capital Ltd, ICICI Securities Ltd, SBI Capital Markets Ltd and Anand Rathi Advisors Ltd

Registrar to the Offer: KFin Technologies Ltd

The Objective of the Issue

- Rs. 138 Cr of the Net Proceeds would be used for repayment of existing debt

- Rs. 60 Cr would be used as Capital expenditure for the purchase of a Plant & machinery.

- The remaining of the Net Proceeds would be used for General Corporate Purposes

Conclusion

As we conclude the article on Azad Engineering IPO Review, We now approach the end of the article hoping to have briefed you about everything you need to know about the Company & its IPO. The Company has its business interests in one of the most lucrative industries in India. Each stock in this industry is valued at an average PE of 77x.

The Company’s revenue growth looks fundamentally strong but those growth rates do not convert to profitability (yet). The weight of the debt eats up a chunk of its profits and its prepayment plans will be the need of the hour.

So what do you think about Azad Engineering? Will it be able to achieve the premium valuations such as its peers? Let us know in the comments below.

Written by Nasir Hussain

By utilising the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investment.