One of the most anticipated IPOs of 2025, National Securities Depository Limited (NSDL), is set to launch its long-awaited IPO following SEBI’s approval to go public and list itself on the Indian stock exchanges. The IPO will open from 30th July to 1st August.

This IPO is going to be a complete offer for sale(OFS), with up to 5.01 crore equity shares being offered to the public by the management. It is to be noted that since NSDL is a professionally managed company, there are no promoters, and the funds raised through the IPO will be diverted to them and won’t be used for corporate purposes.

The entities that are going to sell a part/whole of their stake in the firm are the National Stock Exchange of India(NSE), HDFC Bank, SBI, IDBI Bank, Union Bank of India, and Administrator of the Specified Undertaking of the Unit Trust of India.

Regarding the business, it is one of the only two depositories available in India, alongside Central Depository Services Limited (CDSL), which is already listed on the stock exchanges. So, since NDSL is also going public, it raises a concern to the public and existing shareholders of CDSL about whether to choose CDSL or the newly listed firm NDSL, which could grow their investment. Let’s see what is unveiled further in the article.

Get complete details about the NSDL IPO—including dates, price band, and lot size—on Zerodha. Stay updated with all the latest IPO info Click Here

Central Depository Services Limited (CDSL)

Central Depository Services Limited (CDSL) is an Indian securities depository that enables electronic holding and transfer of financial securities. It offers services like dematerialization, trade settlement, corporate action processing, pledging, and e-voting. CDSL ensures secure, paperless, and efficient capital market operations for investors, brokers, and companies.

CDSL is also a professionally managed firm like NSDL, with major shareholders consisting of BSE (15%), Life Insurance Corporation of India, Nippon India Small Cap Fund, Parag Parikh Flexi Cap Fund, and many others.

It has demat custodies worth Rs. 71 lakh crores, and as of Q4FY24, it derived 33.9 percent of its income from annual issuer income, 22.65 percent from IPO/CA income, 19.14 percent from transaction charges, 14.45 percent from online data charges, and 9.76 percent from other operations.

Coming to market dominance in the number of demat accounts managed, CDSL holds a 76 percent market share with 15+ Crore demat accounts, an impressive growth driven mainly by retail and discount brokers like Zerodha, Groww, and Upstox.

The management is confident in maintaining its leading position, foreseeing India’s capital market growth as well as keeping in consideration the unpredictability of market volumes and regulatory outcomes. It cites 8x growth in demat accounts in 5 years, with strong profit growth and increased brand importance, along with expansion in mutual funds and the insurance segment.

So we just saw that CDSL seems to be doing pretty well in the depository race against NSDL, with a good number of demat accounts in custody with a dominant market share and diversified income across multiple segments, along with the management outlook. Now, let’s see what NSDL has to offer that can portray itself head-to-head against its competitor and attract the public towards its IPO.

National Securities Depository Limited (NSDL)

National Securities Depository Limited (NSDL) is India’s first and largest central securities depository, established in 1996 and regulated by SEBI, with the country’s paper‑based securities system.

It was formed as a direct result of the Harshad Mehta scam of 1992, and its sole purpose was to eliminate risks like bad delivery, forgery, and delays in title transfer by enabling electronic holding, seamless trade settlement, automated corporate‑action processing, and pledging/lending of demat assets, thereby greatly improving market safety, speed, and cost‑efficiency.

It caters to the diverse needs of the securities market in India and introduced several additional products, e-services, and ancillary value-added services and initiatives through NSDL and its subsidiaries, NSDL Database Management Limited (“NDML”) and NSDL Payments Bank Limited (“NPBL”), thereby emerging as a key enabler for the financial market in India.

NSDL derives recurring revenues from Annual Custody Fees charged to Issuers and Annual Fees charged to Depository Participants and other through other services as

- annual fees charged to issuers for foreign investment limit monitoring.

- annual fees from brokers for IDeAS service,

- license fees to DPs for providing its DPM software,

- annual fees from mutual funds towards statement downloads,

- annual fees from SEZ units towards system usage and transaction charges;

- annual fees from insurance companies in relation to credit of policies, and

- annual usage fees for generation of ITP for registration of NSR.

Earlier, NSDL, through its subsidiary NSDL e-Governance Infrastructure Ltd (now renamed Protean eGov Technologies Ltd), used to deliver digital infrastructure services to the government and regulated entities such as Aadhaar E-KYC, E-Signature pan services, identity identification, and many others. Though it was earlier its subsidiary, Protean is now a separate entity and does not contribute a part of NSDL’s revenue, and NSE still owns a stake in it along with other professional managers.

Comparison

Coming back to the depository race, NSDL holds a 24 percent market share in the number of demat accounts held compared to the dominant player CDSL (76%), thanks to its continued business with dominant brokers in the industry.

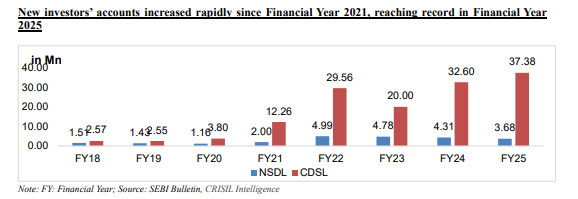

When we look at the trend of new investor accounts being opened, it has rapidly increased since COVID-19, when people had enough time to divert their interest towards the stock market, which led to the Nifty rally from 8,083 levels in April 2020 (post-COVID-19 crash) to 25,062 levels, which grew by 210%.

As part of the new investors trend, the accounts opened across the two depositories grew from 1.16 Mn and 3.80 Mn in FY20 to 3.68 Mn and 37.38 Mn across NSDL and CDSL. CDSL saw the most new accounts opened, which is 10X compared to NSDL, as CDSL works with most of the discounted brokers offering lower charges, be it AMC, free trade delivery, and many more; most turned towards them, leading CDSL to hold the dominant market share with the largest number of demat accounts held.

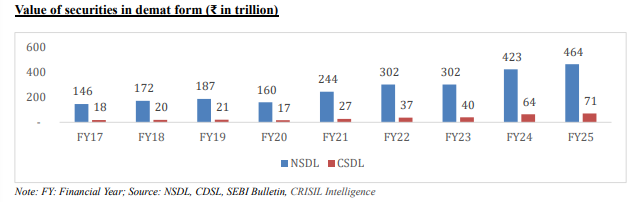

But if we compare it solely on the basis of a market share, we are just looking at the tip of an iceberg. If we look at the quantity of securities held in demat form as of FY25, NSDL holds 4.75 Lakh Crore, which is 5.6x times greater in size than CDSL, which holds 83,600 Crore.

Quantity of securities held in demand form (In Billion)

Following, if we look at the value of securities held in demat form, CDSL holds securities worth Rs. 71 trillion, whereas NDSL holds securities worth Rs. 464 trillion, which is almost 6.5x more than the value of securities held by CDSL.

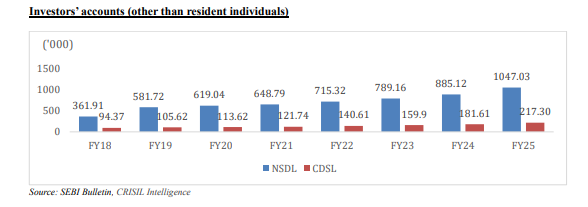

As we discussed earlier, CDSL is the market leader considering the number of demat accounts held, but if we consider the investor accounts held other than the resident individuals, NSDL holds a bigger chunk with a whopping 10.47 lakh accounts compared to 2.17 lakh accounts held by CDSL.

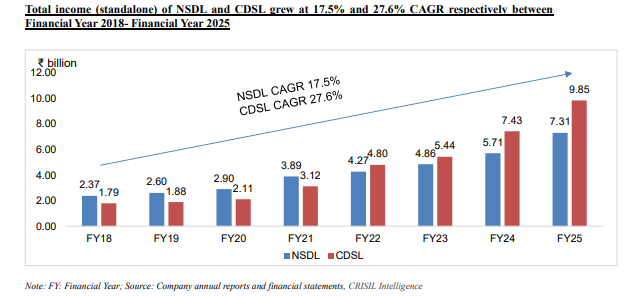

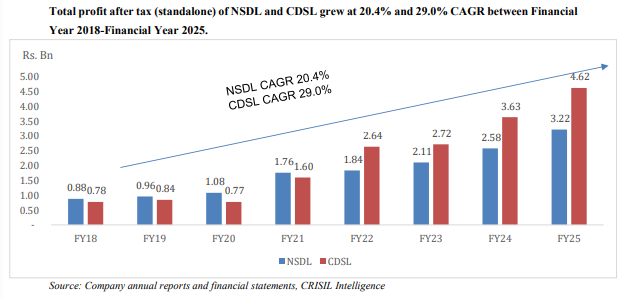

Following the financial performance by going through the data available in the RHP, the total standalone income of NSDL and CDSL has grown at a CAGR of 17.5 percent from Rs. 2.37 billion to Rs. 7.31 billion and 27.6 percent from Rs. 1.79 billion to Rs. 9.85 billion, and coming to profitability, it has grown at a CAGR of 20.4 percent from Rs. 0.88 billion to Rs. 3.22 billion and Rs. 0.78 billion to Rs. 4.62 billion, respectively, from FY18 to FY25, showing better operational efficiency by CDSL.

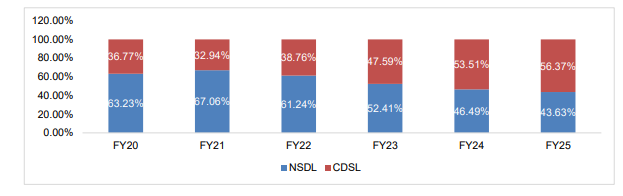

Coming to the operational front, as of FY25, the share of NSDL’s and CDSL’s annual charges and custody revenue in the depositories’ total annual and custody charges stood at 43.63% and 56.37%, respectively. Over the period, NSDL derived a decreasing share from it from 63.23% to 43.63%, whereas CDSL increased it from 36.77% to 56.37% over FY20-25.

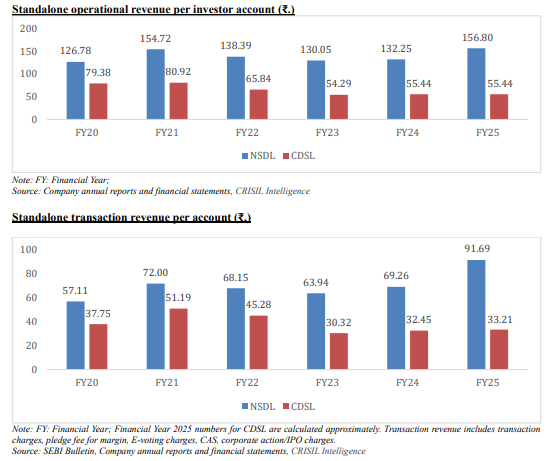

NSDL earns a higher operational revenue per investor and transactional revenue per account, i.e., Rs. 156.80 and Rs. 91.69, compared to CDSL, which earns Rs. 55.44 and Rs. 33.21.

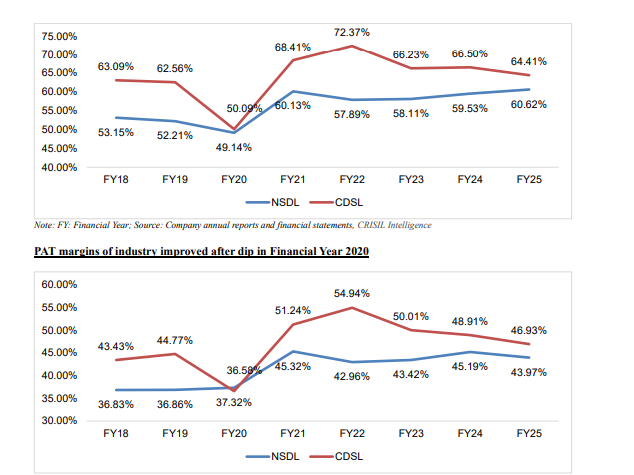

Coming to the EBITDA margins, both experienced a rollercoaster ride from a dip in FY20 (49.14%, 50.09%). CDSL derived higher margins of 72.37% in FY22 and stabilized to 64.41% in FY25, whereas NSDL kept a stable 58-61% margin range. Following CDSL, which made peak margins of 54.94% in FY22 and made 46.93% in FY25, NSDL kept a stable 43-45% range.

EBIDTA margins of industry improved after dip in financial year 2020

Accordingly, looking above, both have performed well in a head-to-head competition over the years by improving their operational efficiency, optimizing their costs and resources, and diversifying into different domains of a similar nature, thereby increasing and expanding their operations and profitability.

Now comes the question is which horse to bet on for the future? Is it the already listed CDSL that dominates the market in number of demat accounts held, diversification in business, consistency in growth and margins, and continued business with the well-growing discount brokers, or NSDL, the “Dark Horse” sitting at the peak, being the choice of big institutional investors, holding 5.6x & 6.5x of the quantity and value of securities held by CDSL?

It may well come down to how you want to play the long game, backing CDSL’s momentum in retail volume and razor‑sharp profitability, or NSDL’s unmatched depth in institutional assets and sticky revenues.” So, will you bet on the proven retail titan or the stealthy institutional giant?

Written by: Bharath K.S