![]()

![]()

Concord Biotech IPO Review: Concord Biotech Limited is coming up with its Initial Public Offering. The IPO will open for subscription on August 4, 2023, and close on August 8, 2023.

In this article, we will look at the Concord Biotech IPO Review 2023 and analyze its strengths and weaknesses. Keep reading to find out!

Concord Biotech IPO Review – About The Company

Established in 1991, Concord Biotech Limited is a biopharma company which is R&D-driven and based in India. The company is one of the worlds leading developers and manufacturers of fermentation-based APIs across immunosuppressants and oncology in terms of market share.

The company has established a global presence and supplies its products to over 70 countries including the USA, India, Europe, and Japan consisting of over 200 customers.

As of FY23, the company has established two DSIR-approved R&D units with 148 members, which includes members having doctoral qualifications.

It has set up 3 manufacturing facilities in Gujarat comprising of API manufacturing facilities in Dholka and Limbasi and a formulation manufacturing facility in Valthera. These production facilities have been divided into 41 manufacturing blocks and 387 reactors at the Dholka and Limbasi sites, giving the company flexibility in plant layout to meet customer demands.

Products by the company:

Following are the different Therapeutic Areas under which the company manufactures its products:

- Immunosuppressants

- Anti-bacterial

- Oncology Drugs

- Anti-fungal

- Others

Industry Overview

As disease patterns evolve from acute to chronic, resulting in high medication (and API) volume consumption, access to healthcare facilities and affordable medicine expands, and financial stability grows, the API sector is expected to expand in unison.

In 2022, the Indian API market was valued at $17 billion, which included APIs manufactured for export as well as APIs used in formulation manufacturing. Of this, $5 billion accounted towards API and $12 billion was attributed to APIs required for formulation manufacture,

Between 2022 and 2026, the entire domestic India API market is predicted to rise at an 11.1% CAGR.

On the other hand, export of the API market is expected to grow at a CAGR of 7% to 9%. The growth rate for exports is expected to be at a lower rate Indian formulation manufacturers expand capacity, reduce import dependence for API, and consume increasing amounts of domestically-produced APIs

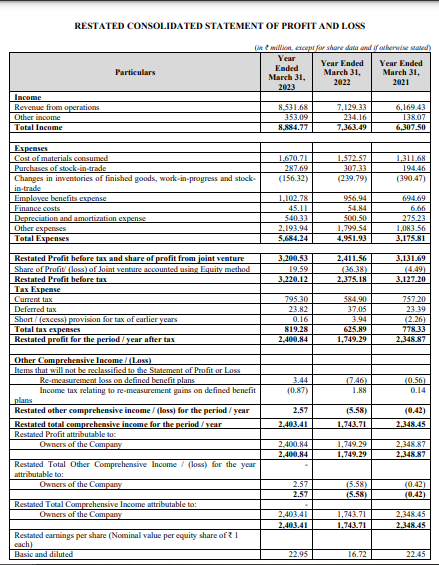

Concord Biotech IPO – Financial Highlights

If we look at the financials of Concord Biotech Limited we find out that their assets have grown from ₹1,182.55 crores in March 2021 to ₹1,513.98 crores in March 2023.

Their revenues also follow a similar trend increasing from ₹630.75 crores in March 2021 to ₹888.48 crores in March 2023. Though there was a steady increase in its revenue, the net profits have only marginally increased from 234.89 crores to ₹240 crores during the same period.

On a positive note, the company has cut down its borrowings from ₹86.35 crores to ₹31.24 crores during FY21 to FY23.

During FY23, the company has reported an ROE and RoCE of 20.06% and 24.27%, respectively. Though these ratios indicate an efficient use of the company’s resources, they have declined compared to FY21.

The balance sheet of the company

Profit and loss Statement of the company

Key Players in the Industry

The following image will show you the listed key players in the industry that can be compared with Concord Biotech Limited:

Strengths of the Company

- The company has established its presence across the fermentation value chain which requires specialized manufacturing expertise. This, combined with complicated technological capabilities, challenges in scaling up operations, and the huge capital investment in equipment and resources necessary, has resulted in a major entry barrier into the fermentation-based API industry.

- In 2022, the company became a major producer of fermentation-based APIs for immunosuppressants and oncology, with over 20% market share. They are expected to continue on the same trajectory with the growth potential in the immunosuppressant drug market.

- The company’s manufacturing facilities in Dholka and Limbasi are divided into 41 manufacturing blocks to process different classes of APIs. This provides a flexible plant configuration and allows us to scale up production volume to meet increased demand.

- Over the years, the company has established a long-standing relationship with certain key customers, including leading global generic pharmaceutical companies. As of FY22, the company has built a base of 200 customers in over 70 countries for both its API and formulation products.

Weaknesses of the Company

- The company’s manufacturing and research facilities are all located in Gujarat. Any factors affecting this geographical location can completely halt or slow down the operations.

- A significant amount of the company’s revenue is based on a small number of consumers. Any major decrease in demand for its products from such clients may have a negative impact on the business.

- As the company derives a significant portion of its revenue from exports, it is subject to risks associated with exchange rate fluctuations.

- As the company has a limited number of customers, it does not have much room to negotiate the prices which are favourable in terms of margins. Thus, it would be difficult for the company to maintain profitability if there is any increase in operating costs

- The company is entitled to incentive schemes like PLI which helps the company smoothly run its operations. The reduction or termination of such schemes or non-compliance with their conditions could adversely affect its business.

Concord Biotech IPO Review – GMP

The shares of Concord Biotech traded at a premium of 27.6% in the grey market on August 1st, 2023. The shares traded at Rs 946. This gives it a premium of Rs 205 per share over the cap price of Rs 741.

Concord Biotech IPO Review – Key IPO Information

| Particulars | Details |

|---|---|

| IPO Size | ₹1,551.00 Cr |

| Fresh Issue | -- |

| Offer for Sale (OFS) | ₹1,551.00 Cr |

| Opening date | 4 August 2023 |

| Closing date | 8 August 2023 |

| Face Value | ₹1 per share |

| Price Band | ₹705 to ₹741 per share |

| Lot Size | 20 Shares |

| Minimum Lot | 1 |

| Maximum Lots | 13 |

| Listing Date | 18 August 2023 |

Promoters: Sudhir Vaid and Ankur Vaid

Book Running Lead Manager: Kotak Mahindra Capital Company Limited, Jefferies India Private Limited and Citigroup Global Markets India Private Limited

Registrar to the Offer: Link Intime India Private Limited

The Objective of the Issue

Following are the Objectives of the issue by the company:

- To increase the visibility and brand image of the company through the issue

- To provide liquidity to the company’s shareholders.

- Achieve the benefits of listing the shares on the Stock Exchanges

In Closing

In this article, we looked at the details of Concord Biotech Review 2023. Analysts remain divided on the IPO and its potential gains. This is a good opportunity for investors to look into the company and analyze its strengths and weaknesses. That’s it for this post.

Are you applying for the IPO? Let us know in the comments below.

Written By Aaron Vas

By utilizing the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks also get updated with stock market news, and make well-informed investment decisions.