Fundamental Analysis Of Syrma SGS Technology: Picture a world where circuits hum with vitality, and innovation sparks life into every electronic device we touch. This is the realm of Electronics Manufacturing Services (EMS), a behind-the-scenes orchestrator of the tech symphony.

In our exploration today, we’re peeling back the layers of this electrifying universe, with a special focus on the distinctive role played by Syrma SGS Technology. In this article, we will conduct a Fundamental Analysis Of Syrma SGS Technology Ltd and analyse the potential outlook of the company.

Fundamental Analysis of Syrma SGS Technology

We’ll begin our Fundamental Analysis of Syrma SGS Technology by becoming acquainted with the company’s operations and products. Following that, we’ll go into the stock’s financials. The article concludes with a highlight of future plans and a summary.

Industry Overview

India is set to become a global leader in electronics manufacturing, playing a vital role in its goal to become a USD 10 trillion economy. The EMS industry in India is anticipated to achieve a market size of US$80 billion in the next five years, with a significant portion of this growth being driven by mobiles and consumer electronics and appliances.

Other sectors, such as lighting, auto, and others, are also expected to contribute to this growth. Over the next decade, India is expected to emerge as a major player in the electronics manufacturing industry, due to the growing domestic demand and enhanced export competitiveness.

The country has witnessed a nearly twofold increase in domestic production between FY17 and FY22, and this trend is expected to continue with a CAGR of 24% between FY22 and FY27.

Company Overview

Syrma SGS is a design-led manufacturing Company with deep expertise in Mobility, Hi-Tech, Healthcare, Consumer, Industrial, and other solutions. Located in Chennai, it is a manufacturer of turnkey Electronic Manufacturing Services (EMS).

The Company’s comprehensive EMS range encompasses everything from product design to quick prototyping, PCB assembly to Box build. Additionally, it also offers customized end-to-end solutions for RFID tags and inlays, high-frequency magnetic components, repair, rework, and automatic tester development services.

The Company has been in the EMS space for over 4 decades now serving 270+ customers across 20 countries. Syrma owns 12 manufacturing facilities and 3 Research & Development labs, with a total plant area of 8.25 Lakh sq ft.

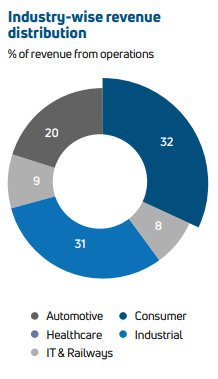

Syrma’s major clients are from the consumer, Industrial, Healthcare, Automotive, and the IT segment. The Company earns 70% of its revenue from the Domestic segment, while exports contribute to 30%.

The following image shows the revenue breakdown of the company from different industries:

Fundamental Analysis of Syrma SGS Technology – Financials

Using the annual reports declared by the company, we will now conduct a fundamental analysis of Syrma SGS Technology Limited.

Revenue and Net Profit Growth

The Income statement of the company indicates that the revenues of the company have increased from Rs.879 Crores to Rs. 2,092 from FY20 to FY23 respectively. This gives the company a 3-year CAGR of 33.51% on its revenue.

During the same duration, the net profits of the company increased from Rs.91 Crores to 123 Crores but grew at a CAGR of 10.57%.

The table below shows the total income and net profit of Syrma SGS Technology Ltd for 4 financial years:

| Year | Total income (Rs in Cr) | Profit after tax (Rs in Cr) |

|---|---|---|

| 2023 | 2092 | 123 |

| 2022 | 1284 | 76 |

| 2021 | 904 | 65 |

| 2020 | 879 | 91 |

| 3-year CAGR growth | 33.51% | 10.57% |

Margin Analysis

While the revenue and profits of the company have increased over the years, the margins of the company show a different picture. We can see that the operating profit margins and the net profit margins of the company are on a declining trend until FY22, with a slight increase in FY23.

This indicates that along with the increasing sales, the company’s operating expenses have also increased. During FY23, the company reported an operating profit margin and a net profit margin of 11.1% and 5.88%, respectively.

The table below shows the operating and net profit margins of Syrma SGS Technology Ltd for 4 financial years:

| Year | Operating Profit Margin | Net Profit Margin |

|---|---|---|

| 2023 | 11.10% | 5.88% |

| 2022 | 10.30% | 5.25% |

| 2021 | 12.90% | 7.26% |

| 2020 | 16.50% | 10.39% |

Return Ratios: RoE and RoCE

The return ratios of the company also follow a similar trend as the operating margins of the company. The ROE and ROCE have declined until FY22 with a slight increase in FY23.

During FY23, the company reported an ROE and ROCE of 11.66% and 14.99%, respectively. This suggests the efficiency at which the company is utilizing its resources and the returns it’s given to the capital invested by the shareholders is below average.

The table below shows the ROE and ROCE of Syrma SGS Technology Ltd for 4 financial years:

| Year | ROE (%) | ROCE (%) |

|---|---|---|

| 2023 | 11.66% | 14.99% |

| 2022 | 9.24% | 11.83% |

| 2021 | 12.84% | 15.28% |

| 2020 | 21.64% | 23.29% |

Debt & Interest Coverage Ratio

If we look at the company’s leverage situation, we can notice that the company has maintained a consistent and a debt-to-equity ratio over the last 4 financial years.

During FY23, the company reported a debt-to-equity ratio of 0.28. This suggests that the company majorly uses its funds to run its business and is also capable of borrowing additional funds for the growth of its business.

During FY23, the company reported an interest coverage ratio of 7.95. This means the company has earned enough profits to cover its interest payments 6 times additionally.

The table below shows the Debt-to-equity & Interest Coverage Ratio of Syrma SGS Technology Ltd for 4 financial years:

| Year | Debt to Equity (x) | Interest Coverage Ratios (X) |

|---|---|---|

| 2023 | 0.28 | 7.95 |

| 2022 | 0.27 | 10.42 |

| 2021 | 0.22 | 9.99 |

| 2020 | 0.28 | 8.37 |

Future Plans Of Syrma SGS Technology

So far we looked at the previous fiscals’ data for our fundamental analysis of Syrma SGS Technology. In this section, we’ll try to make sense of what lies ahead for the company and its investors.

- The Company currently has an order book worth Rs. 3000, which is nearly Rs. 1200 Cr up from the previous year. Syrma aims to execute at least 70% in FY24.

- Syrma has received RDSO’s approval from Indian Railways. Although the current contribution from railways is small, the Company expects more business from railways.

- The Company’s Capex in FY23 was around Rs. 170Cr. In FY24, it planned a capacity of Rs. 200-260 Cr in greenfield expansions.

Fundamental Analysis of Syrma SGS Technology – Key Metrics

We are almost at the end of our fundamental analysis of Syrma SGS Technology. Let’s take a quick look at the stock’s important metrics.

| Particulars | Figure | Particulars | Figure |

|---|---|---|---|

| CMP | ₹ 536.15 | Market Cap (Cr.) | ₹ 10,131 |

| EPS | ₹ 7.51 | Stock P/E | 75.97 |

| RoCE (%) | 14.99% | RoE(%) | 11.66% |

| Promoters Holding | 47.21% | Debt to Equity | 0.28 |

| Net Profit Margin(%) | 5.88% | Operating Profit Margin(%) | 11.10% |

Conclusion

As we conclude our fundamental analysis of Syrma SGS Technology Limited, has shown robust revenue growth over the past 4 years, aided by strong industry tailwinds. Furthermore, the company has a healthy order book and plans for capacity expansions, indicating good growth. However, it is important to monitor the company’s margins closely to ensure that they keep up with the increasing sales.

What are your thoughts on Syrma SGS Technology? let us know in the comments below

Written By Aaron Vas

By utilising the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investments.