Jyoti CNC Automation IPO Review: The Manufacturing sector is running in full swing on the back of increased demand for automobiles and production Linked Incentives (PLI). Make in India and Export to the World is the norm.

All of this is set to benefit the manufacturing sector, but at the same time, this economic scenario will surely spruce up demand for its underlying industry, the manufacturers of Computer Numerical Control (CNC) machines.

These machines are used by manufacturing companies to create complex tools. The CNC machine is a numerically controlled machine that is programmed to create the desired tool with extreme precision.

In this Jyoti CNC Automation IPO Review, we take a look at their operations, financials, GMP, strengths, weaknesses, Peer comparison & more…

Jyoti CNC Automation IPO Review

Today, we talk about about one of the leading manufacturers of these CNC Machines. The Company Jyoti CNC Automation is coming up with its IPO issue of Rs. 1000 Cr which will open on 9th January 2024. The issue will close on 11 January and will be listed on the exchange on 16th January 2024.

About the Company

The Company is the third largest manufacturer of metal-cutting computer numerically controlled (CNC) machines, with a 10% market share in India & 0.4% share globally.

The Company is a predominant manufacturer of 5-axis CNC Machines offering over 200 variants across 44 series. It has a portfolio of CNC Turning Centers, turn-mill centers, and vertical and horizontal machining centers.

Jyoti CNC has over 20 Years of experience designing & manufacturing Tools for Companies in Aerospace, defense, Auto Components, General Engineering, and many more. It supplies to Romania, France, Poland, Belgium, Italy & United Kingdom.

The Company has 3 manufacturing facilities, of which 2 are in Rajkot, Gujarat, and 1 in Strasbourg, France. The facility in Gujarat & France each has their own Research and development center employing 141 employees.

Jyoti’s clients include famous names such as Bharat Forge, Tata Advanced Systems, and Shakti Pumps (India) in the domestic markets. Foreign customers include Bosch Ltd, Turkish Aerospace, and Hawe Hydraulics among others.

The Company’s biggest clients are from the Automotive segment which contributed to 46.68% of its FY23 revenue. Aerospace & defense brought in 20.32% of revenue and General Engineering brought in 19.58%.

Jyoti’s Top 3 clients are responsible for 14% of its FY23 revenue. 16% of the revenue came from its Top 5 Clients and 20.08% of FY23 revenue was paid by the Top 10 clients for the Company.

About The Industry

India’s Index of Industrial Production, which tracks all forms of Industrial activity in India saw the highest monthly growth of 11.4% in July 2023. The index has also expanded by 5.7% since July 2022.

India’s merchandise exports have recovered from the pandemic lows to register the highest-ever annual export growth of USD 447.46 Bn, increasing by 6.03% in a year. A sharp recovery in key markets, increased consumer spending, and increased spending stimulated this demand.

The manufacturing sector in India, to which Jyoti CNC also supplies is poised for strong growth on the back of the China+1 strategy and Production Linked Incentives (PLI) schemes.

India has signed trade deals with UAE worth $100 billion over the next five years from $60 billion in 2022. India and Australia also signed an interim free trade deal in April 2022 which is likely to double bilateral trade from $27 billion in 2022 to $50 billion over the next five years and benefit Indian manufacturing through the availability of cheaper raw materials such as steel, aluminum, and textiles besides enhancing market access.

Jyoti CNC Automation – Financials

Jyoti CNC has grown its revenue by 27% from Rs. 750 Cr in FY22 to Rs. 953 Cr in FY23. The Company has maintained a growth of 27% CAGR since FY21. However, this double-digit growth does not translate into a growth in Net Profits.

The Company just became profitable in FY23 with a Net gain of Rs. 15.06 Cr in FY23, from a Net Loss of Rs. 48 Cr in FY22. The Company’s Net Profits in H1FY24 are only about Rs. 3.35 Cr, which is less than half of its FY23 results.

A very important point to note is that in FY23, the Company reported an exceptional gain of Rs. 30.4 Cr, due to waiver of loan. If we exclude these exceptional gains, the Company would end up in losses of Rs. 15.34 Cr.

The debt-to-equity ratio of the Company stands at 3.25x as of H1FY24. The Company has Current and non-current borrowings worth Rs. 717.11 & 104.29 Cr respectively. The Debt-equity ratio has however reduced from 19.25x, but remains quite above the highly leveraged zone.

Looking deep into its balance sheet we see that the Company holds inventory worth Rs. 868.35 Cr, which is nearly 50% of its total assets. The Company also has a very low inventory turnover ratio of just 0.48x as of H1FY24.

Key Players

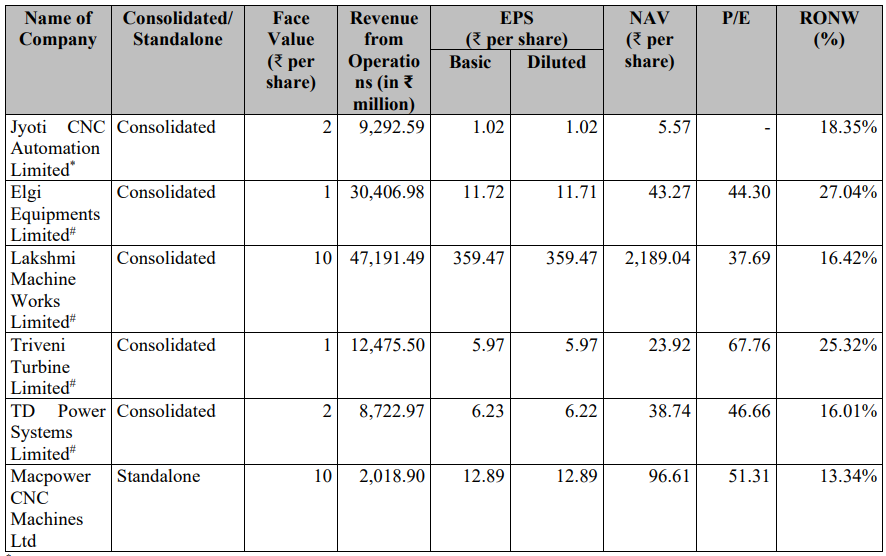

When Jyoti CNC is compared against its peers, it ranks as the 3rd largest on the list. However, the Company has one of the lowest earnings per share as well as the lowest Net Asset Value.

With the max price band of Rs. 331, the Company trades at a sky-high PE ratio of 324x. Take a look below to see how Jyoti CNC compares against its peers.

Strengths of the Company

- One of the leading CNC machine manufacturers in India & globally, with a diverse range of products specialized for multiple industries.

- The Company is diversified across business segments comprising Aerospace, Automotive, general engineering, EMS & dies & molds

- The Company’s integrated manufacturing units ensure that all parts of manufacturing are housed internally, requiring no third-party input.

- As of Q2FY23, the Company had an order book of Rs 3,315 Cr., of which Rs. 1896 Cr is from the Aerospace & Defense segment.

Weaknesses of the Company

- The Company’s Top 3 clients alone brought in 32% of revenue in H1FY24 & 13.95% of revenue in FY23. We see that the Company’s exposure to its biggest clients has increased in the latest Quarters.

- The Company’s debt to equity of 3.25x is a hanging sword on its balance sheet. Debt to debt-to-equity ratio above 2x makes the Company significantly leveraged

- Jyoti CNC turned profitable in the recent FY23 itself. However, the rate of profit growth in the first half of been really slow.

- 50% of the Company’s total assets are stuck in inventory. The Company also had a very slow Inventory Turnover ratio.

- Statutory Auditors of the Company have stated concerns over the Company’s subsidiaries which have accumulated losses over the previous year which eroded their net worth.

Jyoti CNC Automation IPO Review – GMP

The shares of Jyoti Automation CNC Ltd traded at a 25.68% premium in the grey market on January 5th, 2024. The shares in Grey Market traded at Rs 416. This gives it a premium of Rs 85 per share over the cap price of Rs 331.

Key IPO Information

| Particulars | Details |

|---|---|

| IPO Size | Rs. 1000 Cr |

| Fresh Issue | Rs. 1000 Cr |

| Offer for Sale (OFS) | - |

| Opening date | 9 January 2024 |

| Closing date | 11 January 2024 |

| Face Value | Rs. 2 |

| Price Band | Rs. 315 - Rs. 331 |

| Lot Size | 45 Shares |

| Minimum Lot Size | 1 (45 Shares) |

| Maximum Lot Size | 13 (585 Shares) |

| Min. Investment | Rs. 14,895 |

| Listing Date | 16 January 2024 |

Promoters: Parakramsinh Ghanshyamsinh Jadeja, Sahdevsinh Lalubha Jadeja, Vikramsinh Raghuvirsinh Rana, and Jyoti International

LLP

Book Running Lead Manager: Equirus Capital Private Ltd, ICICI Securities Ltd & SBI Capital Markets Ltd

Registrar to the Offer: Link Intime India Pvt Ltd

The Objective of the Issue

- Rs. 475 Cr off the net proceeds of the Issue will be used towards prepayment of certain debt availed by the Company.

- The rest of the Capital will be used towards funding the Term Working Capital requirements of the Company and general Corporate Purposes.

Conclusion

We have now reached the end of Jyoti CNC Automation IPO Review having briefed you on what the Company does, how much market share it has in India & what opportunities lie ahead for the Company. In our view, the Company does have good revenue growth, but the Profit Margins do not match these numbers.

The Profits reported in FY23 also do not count as these are part of exceptional gains. This coupled with the high debt will remain a risk for the investor to be aware of. So would you take the risk & apply for the IPO? If so, tell us what you find most interesting about the Company, in the comments below.

Written by Nasir Hussain

By utilising the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investment.