Synopsis: With approximately 64% of India’s Global Capability Center (GCC) space being leased out from South India, this region is by far the largest contributor to the country’s GCC market. South Indian cities have become significant hubs for multinational companies, leading to job creation, innovation and a transformation for India’s commercial and residential real estate.

GCCs (Global Capability Centers) are no longer just back office support units – they are now core innovation, R & D and decision making centers for global corporations. South Indian cities clearly stand out due to the technology ecosystem, deep talent pools and superior infrastructure. The cities of south India are capturing two thirds of GCC activity that had a profound impact on urban growth and real estate markets.

The core of GCC dominance: South Indian Cities

Bengaluru – India’s GCC Capital

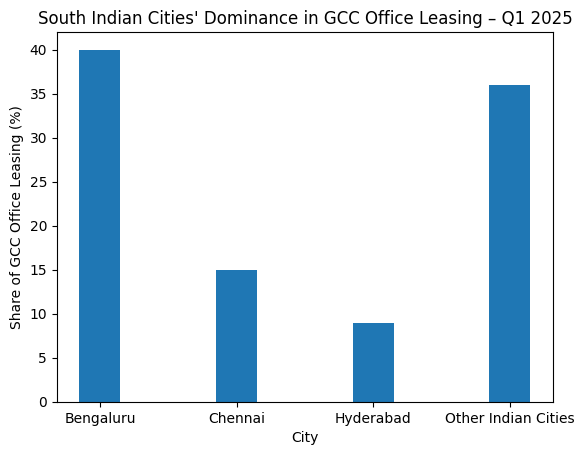

Bengaluru alone contributes about 40% of India’s total GCC office leasing making it the single largest GCC hub in the country. The city hosts advanced GCCs focused on AI, product engineering, cloud computing and deep tech R & D. Major corridors such as Whitefield, Outer Ring Road and Sarjapur Road have transformed into high density employment zones. Nearly 3.3 million sq. ft. leased in Bengaluru with 40 % approx share contributed to India’s GCC leasing.

- Real estate impact: Strong rental demand, sustained price appreciation and premium valuation near metro connected tech hubs. Price appreciation is expected to rise 8 – 11 % over 5 years with 40 % CAGR and rental growth to 6-8 % annually.

Hyderabad- The Fastest Scaling Challenger

Hyderabad attracts around 9% of GCC leasing but its growth momentum is among the fastest in India. The city attracts large campus style GCCs in BFSI, digital services, pharma and cloud platforms. HITEC City, Gachibowli and the financial district have become magnets for global occupiers. Nearly 0.75 – 0.8 million sq. ft. is leased among that 9% share is contributed to India GCC leasing.

- Real estate impact: Competitive entry prices, rapid rental growth, and strong capital appreciation potential over the next decade. Expected residential price CAGR is 7-9 % with rental growth 6-7%.

Chennai- Engineering & Manufacturing GCC Hub

Chennai contributes around 15% of India’s GCC office leasing, giving it a crucial role in South India’s 64% share. It is a preferred destination for engineering, automotive, electronics, and industrial R & D GCCs. The OMR corridor and southern suburbs continue to attract steady, long term occupier demand. Nearly 1.22 million sq. ft. leased in Chennai and 15% share was contributed for India’s GCC.

- Real estate impact: Stable appreciation, lower volatility and consistent rental absorption driven by long tenure GCCs. Expected residential price CAGR is 6-8% with rental growth of 5 – 6%.

City wise GCC Concentration (indicative)

| City | Share of India’s GCCs approx. in % | Key strengths |

| Bengaluru | 35 – 40 | Deep tech, R & D, product engineering |

| Hyderabad | 15 – 18 | Digital, cloud, pharma & BFSI |

| Chennai | 8 – 10 | Engineering, automotive, manufacturing IT |

| Coimbatore | Growing | Cost efficient tech & analytics |

| Kochi | Growing | Fintech, design, mid size GCCs. |

Also read: How GCC Hiring is Boosting the Mid-Income Housing Demand in Tier-2 Cities

Other Indian Cities- The Remaining 36%

Cities such as Pune, Delhi NCR and Mumbai together account for the remaining approximately 36% of GCC leasing. These markets benefit from GCC expansion but lack the scale, clustering effect and depth of tech talent seen in South India. GCC activity here is more fragmented and often focused on niche functions rather than large integrated hubs. Nearly 3 million sq. ft. is leased for GCC office space and it contributes 36% share of India GCC leasing.

GCCs Office leasing

Overall leasing share: In the Q1 2025 South Indian cities accounted for nearly 64% of all GCC office space leased across India’s top 7 cities. Sector wise distribution of leasing IT / ITeS has 35%, BSFI 22%, Manufacturing & industrial 13%, E-commerce 6%, consulting 5% and others 19%.

Why South India Continues to lead

- South India has large pools of engineering, AI, data science and product talent with long standing IT and R & D ecosystems.

- Bengaluru, Hyderabad and Chennai have embraced the captive center model much earlier than other regions having strong clustering effect, easier scaling and hiring, and emerged with vendors, startups and innovative networks.

- South India has good infrastructure & global connectivity with international airports with strong global links, established IT corridors and large Grade A offices.

- These cities are engaged in scaling large multinational operations. It acts as India’s innovative engine for global firms.

- Rising demand for AI, semiconductor design, sustainability tech and cybersecurity.

GCC Growth in Next 5 Years

South India is expected to retain over 60% GCC share by 2030. Tier 2 cities like Coimbatore, Kochi and Trivandrum will absorb overflow demand. GCCs will drive premium office demand, high end housing, and urban infrastructure growth with strong positive spillover into real estate, startups, and local employment. It provides employment opportunities with average GCC salary bands that are 25-40% higher than IT services. The cities have better infrastructure, faster metro & road upgradation.

Conclusion

South India’s 64% dominance in India’s GCC ecosystem is not a short term phenomenon; it reflects decades of ecosystem building, policy support and talent development. Bengaluru leads as the innovative powerhouse, Hyderabad accelerated as the high growth challenger and Chennai anchors stability with engineering excellence. South India remains the strategic heart of global enterprise operation in India driving long term economic growth and consistently outperforming in real estate and urban development.

Written by Soumya M