Synopsis: This article breaks down two of the most debated investment options, real estate and equity, which give more return in 2025 in different areas and key reasons for development and tell you how they performed during market downturns.

In 2025, real estate significantly outperforms equities in India. The residential housing market delivered a robust 15% annual return according to the 1 Finance Housing Total Return Index (TRI), while the stock market struggles with negative returns, the Sensex fell 4.51% and Nifty 50 declined 4.22% from their peaks in September 2024.

Why Real Estate is Leading in 2025

Infrastructure Driven Growth: The connectivity projects are behind the significant price appreciation seen by major metro cities across the nation.

- Delhi NCR, massive 72% jump in luxury home prices, 54% growth in mid-range and premium housing, and 48% rise in the affordable segment,

- Pune Central surged 21% because of the Swargate-Katraj Metro extension.

- The city of Bengaluru has witnessed a massive 24% price surge as a result of the Namma Metro Phase 2 becoming operational.

- Hyderabad has recorded an increase in prices of 31% due to the Regional Ring Road (RRR) project.

- The Aqua Line metro in Mumbai contributed to a 13% hike in prices in the central suburbs of the city.

Market Size and Transactions: The residential sector witnessed an impressive transaction of Rs 1.52 lakh crore during Q3 2025 and a sale of 350,612 units through the major markets in 2024, which is the highest in 12 years and corresponds to a 6.54% year-on-year growth. The luxury market with homes costing over ₹10 million will not only be the primary driver but will also increase by 29% year-on-year, thus, comprising 46% of all sales. The different cities have varying but always strong appreciation:

- Kolkata has 16% year-on-year growth

- Chennai is in second position with 14% appreciation

- Delhi NCR and Bengaluru each recorded a 13% increase

- Hyderabad reached a staggering 80% price growth over the years up to 2025, making it the city with the highest ROI.

Also read: 5 Fast-Rising Karnataka Cities Beyond Bengaluru That Will Become the Next Big Hotspots by 2032

Real Estate vs Stock Market in 2025

| Factor | Real Estate | Stock Market |

| 2025 Returns | 15% annual | 5% |

| Liquidity | Low – weeks,months, years to sell | High- minutes to exit online |

| Initial Investment | Large, typically more than ₹30 lakhs | Low (₹100 SIP possible) |

| Long-term Capital Gains Tax | 20% with indexation | 10-15% on gains over ₹1.25L |

| Risk Profile | Front loaded | Market Volatility, but diversifiable |

| Leverage Potential | High (3-6x typical) | Limited (margin trading restricted) |

| Passive Income | Retail yield ₹30k-36k/ month typical | Dividends variable |

| Entry Barriers | High – stamp duty, registration, GST costs | Low – demat account easily accessible |

The Verdict

For immediate 2025 returns, real estate wins decisively with 15% appreciation against lower equity market returns. However, this comparison requires context:

- If you have strong infrastructure connections and market knowledge: Emerging tier-2 cities like Pune which is 8-12% appreciation, Ahmedabad, and Kochi offer better risk-adjusted returns than saturated metropolitan markets like Mumbai, Bengaluru.

- If liquidity is important: Stock market investments remain superior despite current headwinds, as they can be liquidated within minutes.

- If you can access leverage: Real estate’s 3 to 6x leverage amplifies already-strong price appreciation, making it more attractive for those with strong financial positions.

- For passive wealth building: Equity mutual funds with disciplined SIP strategies provide more sustainable long-term returns (25-33% historical CAGR for select schemes) without the illiquidity burden of direct property ownership.

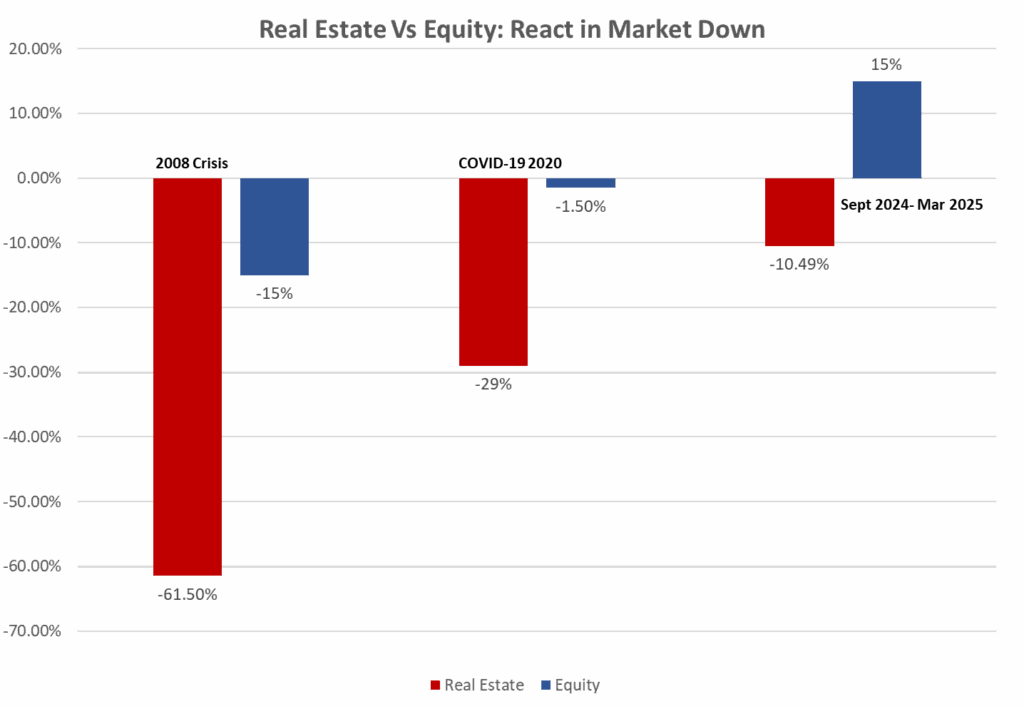

Volatility Characteristics

- Stock Market Volatility: Equities demonstrate very large movements in the short term. The elections in 2024, for example, caused daily dramatic swings in the market. The stock market’s standard deviation of returns was very high in crisis periods and among the reasons was the distress in the realty sector of the index which recorded very high volatility during COVID-19, but this was due to paper loss anxiety rather than asset value destruction.

- Real Estate Stability: A decade of research has demonstrated that property prices in the major Indian cities show an average annual appreciation of 7-10% with very low year-to-year volatility. When there are downturns in the market, the real estate sector merely stops its appreciation instead of reversing sharply. During the pandemic, for example, the property prices were stable to slightly down rather than undergoing the cascading 20-30% corrections typical in the stock market.

Also read: India’s New Rent Rules 2025: Lower Deposits, Stronger Tenant Rights and More

Recovery Speed

Stock Market Recovery: Stocks regain their value quickly, but the market tone is still very uncertain. The 2008 crisis was followed by a big jump in the stock prices which were at the 2011 level but the investors had to go through a lot of false rallies and were anxious most of the time. The COVID-19 crash was a series of a few months in which the market was back as the banks poured in money, but that was only after huge losses in wealth. The current investors in the market are not sure whether the 2024-25 slump is an indication of a deeper correction or a mere temporary pullback.

Real Estate Recovery: The Property markets take longer to recover but do so in a predictable manner. In the case of the financial crisis of 2008, real estate took over 5 years for full recovery, yet it was a gradual and sustainable appreciation curve rather than a series of price fluctuations. Post-COVID, the increase in property values was also slow but steady – tens were not only stable as from Q3 2020 but also resumed by Q4 2020 when there was already appreciation getting deficient in the depressed phase.

Conclusion

The perfect investment approach is the one that mixes both: the use of real estate as a source of safe and steady wealth through long-term inflation with the help of leverage, and the use of equities for their liquidity, tax efficiency, and the role they play in diversifying a portfolio that has been balanced.

Written by Yatheendra N